Medicare 101: The ABCs of Medicare, Whos and Hows of Funding

CATEGORIES

COMPANY TYPE

Medicare may be a public health care option, administered through federal and state programs, but the insurance industry has its own sets of wraparound and replacement policies. For those dipping their toes into the pond of Medicare, we’re covering the basics of the program and what private insurance plans are and do.

Medicare is a federal-state joint program that pays for major medical health care for those over age 65, administered by the Center for Medicare and Medicaid Services (CMS). For consumers, the basic premise is, funded by payroll taxes, the program covers about 80 percent of most health care expenses for surgeries, hospital stays, and other vital coverage as long as the hospital or facilitative care stays are short enough in duration that they don’t become an official long-term-care stay. Medicare is split into Parts A and B, and then, via private insurance, rolls through Plans C to N.

If you’re a U.S. citizen and you or your spouse qualifies for Social Security or railroad retirement benefits, or you’ve paid any amount of Medicare payroll taxes over the years, or you have certain disabilities, you qualify for some kind of participation for Medicare.

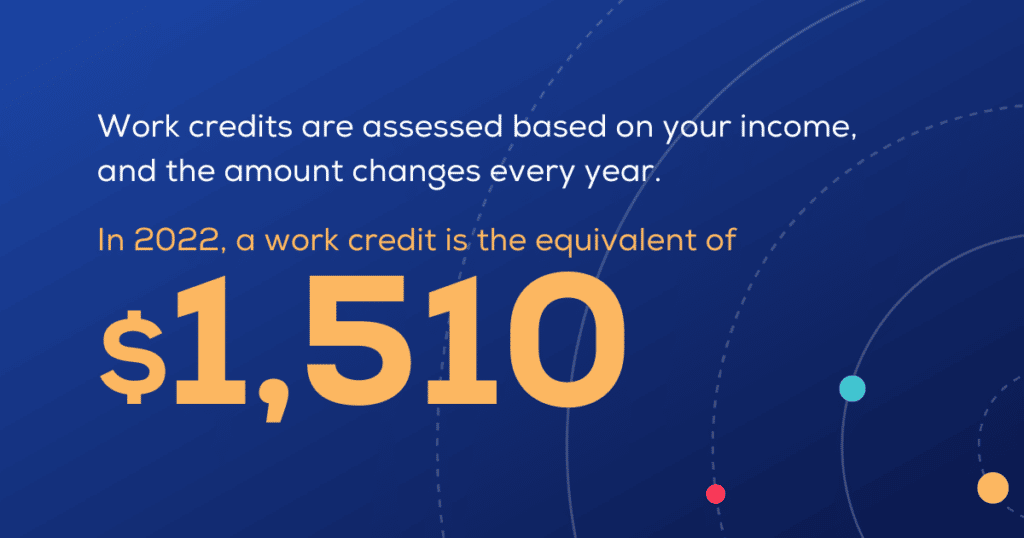

Most Americans fully qualify as long as they’ve worked for 40 “work credits” … work credits are assessed based on your income, and the amount changes every year. In 2022, a work credit is the equivalent of $1,510.

Even those who don’t have sufficient work credits can buy into Medicare or qualify based on other factors, something the AARP covers extensively here. So, tl;dr, most U.S. citizens will qualify for Medicare.

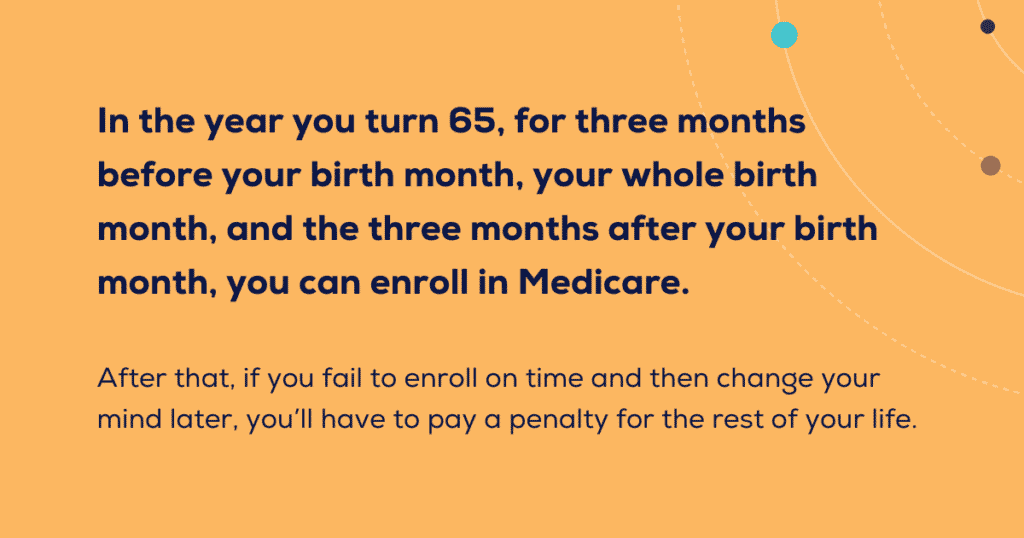

In the year you turn 65, for three months before your birth month, your whole birth month, and the three months after your birth month, you can enroll in Medicare. After that, if you fail to enroll on time and then change your mind later, you’ll have to pay a penalty for the rest of your life.

If you’re covered by traditional group insurance because you or your spouse is still working at age 65, you may only need to sign up for Part A, or explore a situation where your private plan pays first and Medicare pays second.

While there are many other enrollment options and scenarios based on factors like disability status, we’re going to pretty exclusively look at a “typical” 65-year-old enrollment scenario.

Medicare gets confusing because of the differences between public and private insurance and the fact that different aspects of Medicare might have multiple monikers and everything is ruled by an alphabetical shorthand. So, let’s nip this confusion in the bud and explore the alphabet soup of Medicare.

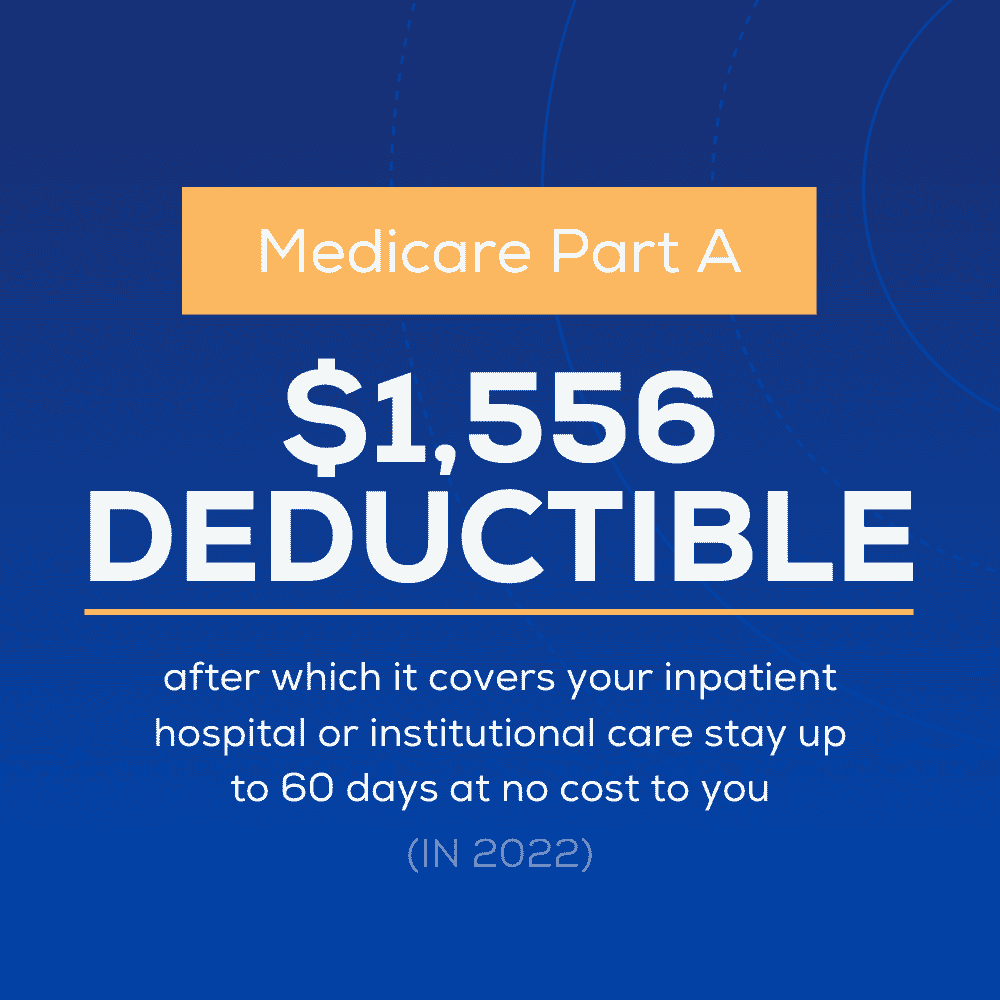

Medicare Part A: Part A is hospital insurance. This is part of “Original Medicare,” and generally doesn’t require a premium payment. Part A has a deductible – $1,556 in 2022 – after which it covers your inpatient hospital or institutional care stay up to 60 days at no cost to you. After 60 days, Medicare requires you to pay daily co-insurance. After 150 days of inpatient care, Medicare will no longer cover a continuous care stay as it deems you will have moved on to a long-term care scenario beyond the scope of Medicare coverage.

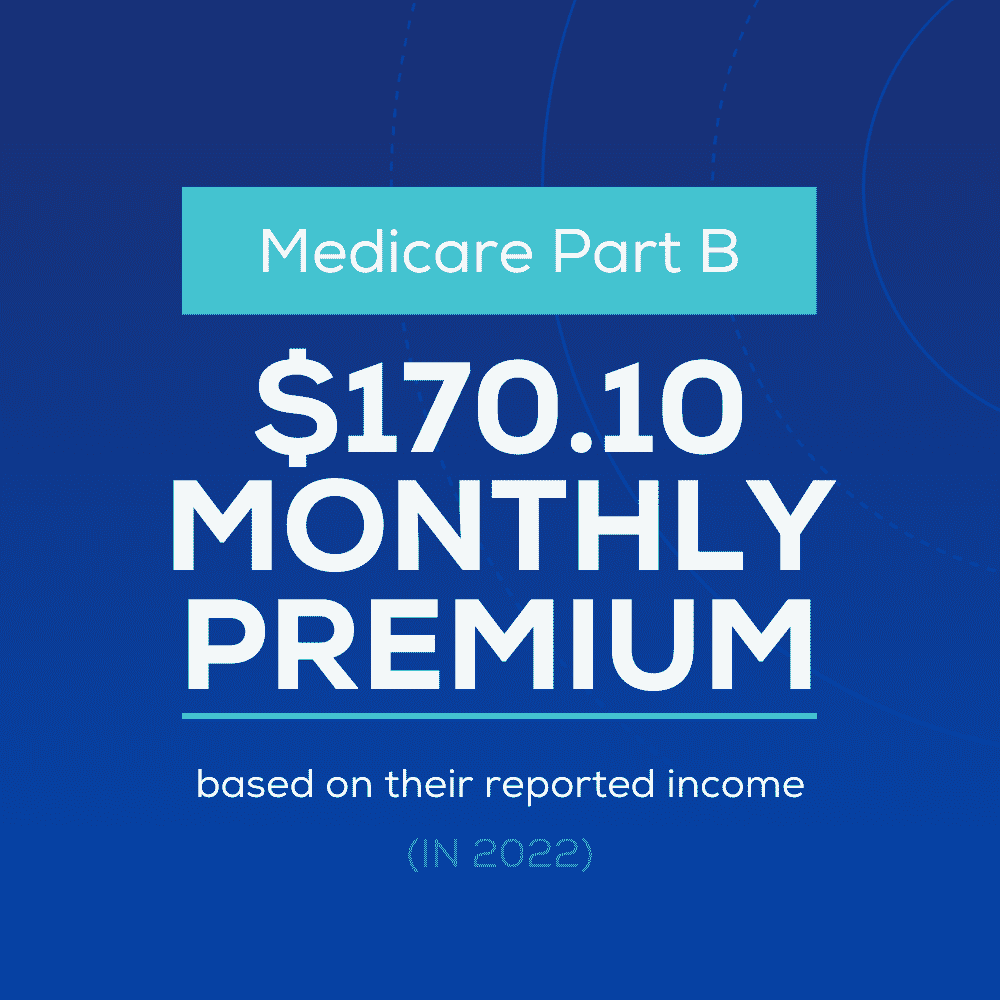

Medicare Part B: Part B is medical coverage and is also part of Original Medicare. What it covers depends very much on what your state and local processing centers consider medically necessary. Generally, preventative screenings and vaccinations are covered, but what Medicare doesn’t cover are preventative wellness checkups. Medicare Part B recipients usually have a monthly premium based on their reported income – most pay $170.10 in 2022, according to CMS. Since many Medicare beneficiaries are already receiving Social Security benefits, CMS automatically deducts premiums from beneficiaries’ Social Security check each month. If you are one of those people delaying Social Security, you will have to pay your Part B premiums out of pocket.

If you have Original Medicare – Parts A and B – then CMS also requires you to purchase a privately administered Part D plan for prescriptions, which we’ll cover further below. Original Medicare also doesn’t cover services like routine dental, vision, or hearing care.

Medicare Part C: Medicare Advantage and Part C are the same thing. This is a private alternative to Original Medicare and so, like private health insurance plans, works via health maintenance organization (HMO) or preferred provider organization (PPO) networks, and may require pre-authorization (limitations that don’t exist via Original Medicare). In exchange for these limitations, Advantage plans also offer more covered services beyond those of Original Medicare. Many Advantage plans include the benefits that would otherwise be covered by a Part D prescription plan, and may also include bells and whistles such as hearing aid coverage, dental, vision, and even gym memberships or food boxes. The variations of Plan C/Advantage coverage are numerous, with no two plans looking the same. Each year during the annual Medicare Advantage Open Enrollment period – January through March – Advantage members can switch plans if they find an Advantage plan that has more appealing benefits.

Medicare Part D: Part D plans offer prescription coverage. While CMS requires Medicare recipients to enroll in Part D, this is private insurance coverage, so it’s important for beneficiaries to find a plan that works best with their specific prescription needs. Those who have Part A and B coverage will also necessarily have Part D, and some Advantage (Part C) members may have coverage that still necessitates Part D, as well. Like Advantage plans, you can switch plans during the open enrollment season.

If you’ve heard of plans like “Plan G” or “Plan M,” those are Medicare Supplements, which may also be known as gap or Medigap plans. Essentially, they are private plans that provide additional coverage around Original Medicare for an additional premium.

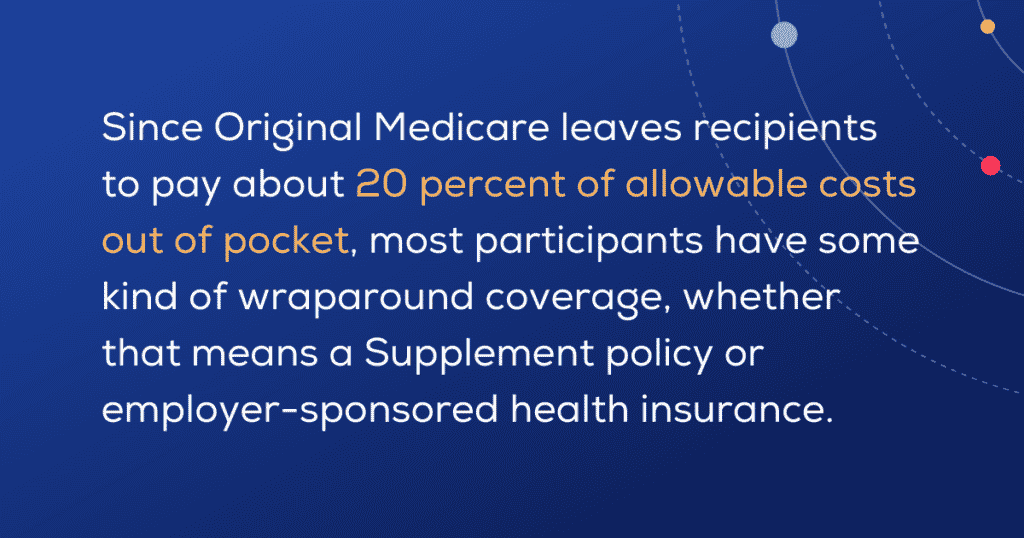

Since Original Medicare leaves recipients to pay about 20 percent of allowable costs out of pocket, most participants have some kind of wraparound coverage, whether that means a Supplement policy or employer-sponsored health insurance. Medicare Part C, or Advantage, participants will not have Supplement plans.

These Supplement policies are standardized, with each letter covering a set menu of benefits. So, Plan N will cover Part A and Part B coinsurance payments, Part A’s deductible, and 80 percent of a foreign travel emergency regardless of what insurance company offers that plan, or what state it’s in. The cost may vary based on an insurer’s marketing efforts and customer service practices – after all, you may want to talk to a real person and not sit on hold for hours – but otherwise a Plan [insert letter] is the same everywhere. And, despite being private insurance, MedSup plans are also required to go wherever Original Medicare is accepted – no networks, no prior authorizations.

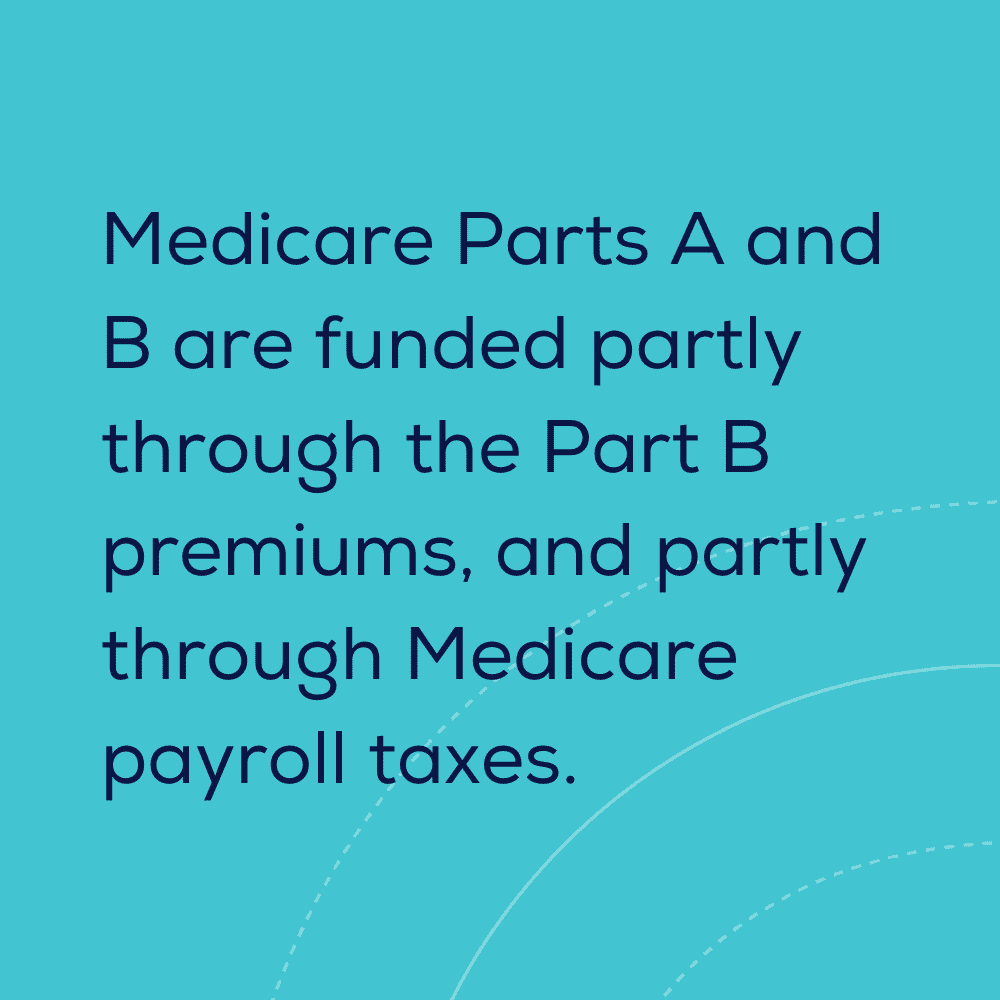

Medicare Parts A and B are funded partly through the Part B premiums, and partly through Medicare payroll taxes. The same Federal Insurance Contributions Act (FICA) taxes you’ve been paying since that first taste of sweet, sweet taxpayer income, the same FICA contributions that run Social Security, also fund Medicare.

Medicare Supplement plans are sustained via premium payments, as are Part D, since they’re all straight up private plans.

Medicare Advantage is largely paid for out of the Centers for Medicare and Medicaid Services (CMS) budget. Each year, Medicare sets a benchmark for what they estimate the per-person spend to average, and Advantage plans “bid” a price that they’ll pay for each member’s care. If their bid comes in under the Medicare benchmark, then the Advantage plan will be paid the per-person bid, plus a rebate, for each person enrolled in their plan.

Many Advantage plans cost participants their Part B premium, which often comes straight out of their Social Security check, and so many marketing materials refer to them as “$0 premium” plans (although they aren’t $0 – that Part B premium is real). Put another way, regardless of whether a person has a Medicare Advantage plan or Original Medicare, the Part B premium will come out of their Social Security check. Advantage plans that don’t come in at or under the CMS acceptable bid cost may charge premiums in addition to collecting the Part B premium.

There are a few reasons premiums have risen. For one thing, the cost of healthcare typically inflates faster than the rest of the economy, so Part B premiums have risen accordingly to keep up with the cost of care. However, this last year a very particular factor was at play in jumping Medicare premiums by almost 15 percent.

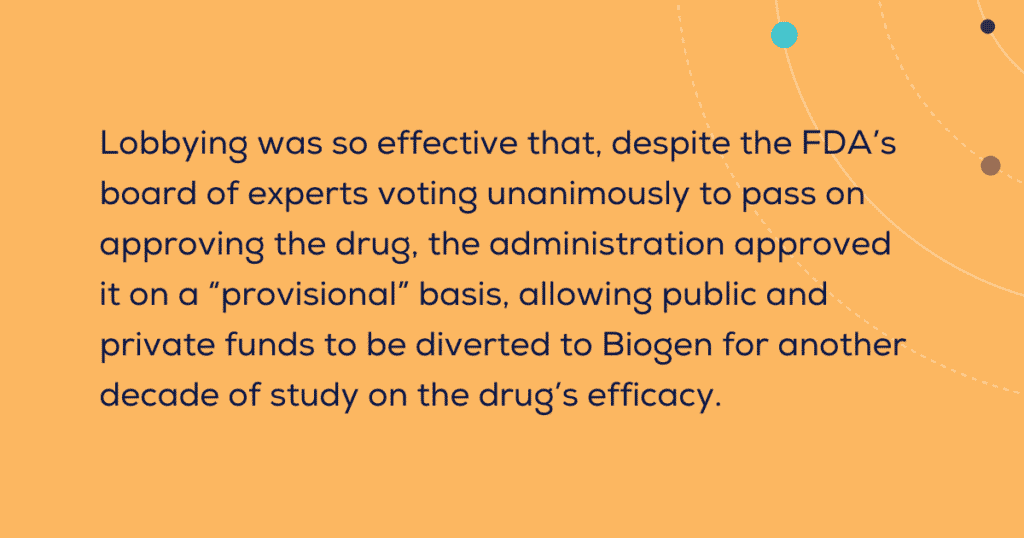

A drug based on monoclonal antibody research (in case you had a COVID-19 bingo card) gained Food and Drug Administration (FDA) approval for treating Alzheimer’s disease, which champions hailed as one of the first breakthroughs for the disease. However, further inspection of Biogen’s Aduhelm hinted the treatment might be dangerous. And ineffective. And pricey (to a tune of $28,500 a year). Despite these drawbacks, the lobbying effort in favor of this drug that even might offer hope for Alzheimer’s patients has been heavy.

In fact, lobbying was so effective that, despite the FDA’s board of experts voting unanimously to pass on approving the drug, the administration approved it on a “provisional” basis, allowing public and private funds to be diverted to Biogen for another decade of study on the drug’s efficacy.

When CMS had to publish the data for 2022’s premiums, the drug’s approval was still in the air. So CMS administrators decided to hedge their bets and increase premiums by over $20 a month, anticipating that Medicare may be on the hook for an almost-$30,000-a-year drug to treat a disease that afflicts more than 5 million Medicare recipients.

Ultimately, after FDA granted provisional status and CMS officials reviewed the data, CMS limited Medicare funding of Aduhelm to trial subjects. A recent statement from the U.S. Department for Health and Human Services said Medicare Part B premiums will be “adjusted downward” next year to reflect that Aduhelm and its high sticker price didn’t ever make it into wider coverage.

While most Medicare recipients use Original Medicare with Part D and some kind of supplemental or gap coverage, that approach has higher premiums than a Medicare Advantage plan that offers everything in one for the same premium cost as Part B.

However, the private insurance approach hasn’t delivered on its promise of outstanding care for lower prices.

Yet, as a spokesperson for the National Association of Health Underwriters discussed at the 2022 Medicarians event, Medicare as a social insurance program is too important and too popular to simply eliminate. So, whether we see increases in Medicare Advantage adoption, or extended regulations to ensure fair coverage, or increased FICA payroll tax limits, the chances are that Medicare will be around for the future.

Digital adoption also holds transformative promise; tools that can pair the best of human relationships and digital tech may hold the key to increasing health outcomes and decreasing the administrative costs of the program.

Now that you know more than you wanted to about Medicare, you can peek at the blog to find more compelling 101 content on non-Medicare topics, or see how AgentSync can help you reduce risks and costs all while streamlining your people teams and digital tools.

Get the latest updates on new insurance industry content.

There are many compliance risks that can put an insurance agent…

You can reduce the risks to your core business!

Let Susan in Compliance finally take a vacation.