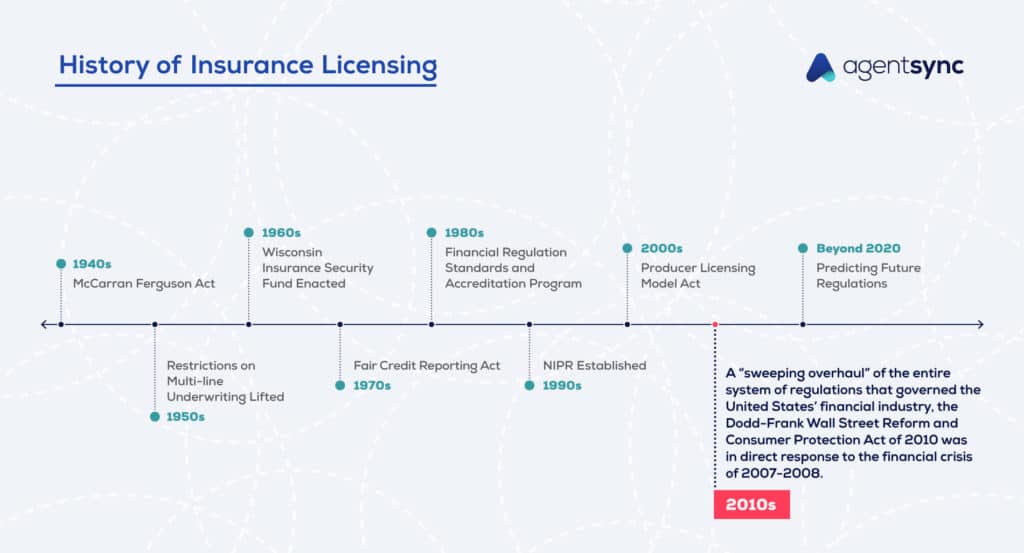

History of Insurance Regulation In The 2010s

CATEGORIES

COMPANY TYPE

Over the past decade alone, there have been a number of extremely significant new laws pertaining to how the insurance industry is regulated. Many of the changing regulations in the insurance industry over the past 10 to 15 years have focused on consumer protection. The events of 9/11 and the Great Recession shone particular light on how vulnerable everyday Americans were to the inner-workings of the financial industry.

With each new presidential election the pendulum swings back and forth. Some administrations have been more focused on protecting consumers at the expense of the free market and insurance company profitability. Others have deregulated the insurance industry, leaving state departments of insurance to take charge of protecting consumers. The 2010s were largely characterized by the presidential administration of Barack Obama, which took an involved approach to regulation. Under President Obama, Congress – as well as state legislative bodies – passed a number of substantial laws that govern insurance business still today.

President Obama’s Affordable Care Act sought to solve the problem of health insurance access and affordability for millions of Americans. By establishing minimum essential services that health insurance companies must cover, and by eliminating pre-existing condition exclusions, gender-based price differences, and lifetime benefit maximums, The ACA opened access to millions of newly insurable individuals. It also brought unprecedented levels of regulation to the health insurance market.

A “sweeping overhaul” of the entire system of regulations that governed the United States’ financial industry. This law was in response to the financial crisis of 2007-2008 and aimed to impose greater regulations on those companies who were onced deemed “too big to fail.” The most stringent rules would apply to a new designation of “systemically important financial institutions,” which often included insurance companies.

This piece of the Dodd-Frank Act had a particularly large impact on the insurance industry. Prior to its enactment in 2011, each state could impose its own eligibility requirements relating to surplus lines of insurance for non-admitted insurers. The NRRA established national, uniform standards that limited the ability of states to tax and regulate surplus lines insurance policies.

In 2011, the National Association of Insurance Commissioners (NAIC) changed its requirements for large amounts of collateral on alien reinsurers. Previously, non-U.S. reinsurers had to provide prohibitively large amounts of collateral – often more than 100 percent of the cost of the risk they were reinsuring! The result of these lower collateral requirements was a dramatic increase in access to reinsurance markets across the world for U.S. insurance companies.

This rule, part of the greater Employee Retirement Income Security Act (ERISA) aimed to increase consumer protection by requiring plan participants to be given written disclosure statements related to fees, conflicts of interest, and many other “fine print” items generally benefitting investment brokers more than their clients. While it was originally introduced by the Obama administration in 2015, the rule faced many challenges and enforcement was postponed. Recent news (as of early 2021) indicates that President Joe Biden will allow the rule to take effect, thus increasing regulation and expenses for those involved in insurance-related investment products.

When it comes to life insurance products, the industry often faced challenges relating to the level of reserve funds on hand. In some instances, the formulas used to calculate required reserves resulted in either largely over-funded or grossly under-funded reserves. In 2017, the National Association of Insurance Commissioners (NAIC) developed a solution through which each insurer’s reserve requirements are based on its own unique information.

Although the administration of President Donald Trump largely cultivated a reputation for deregulation, at the president’s urging, the Department of Health and Human Services, the Department of Labor, and the Department of the Treasury jointly issued a rule in late 2020 meant to standardize the way health insurers and hospitals disclose their pricing and cost-sharing agreements. In an effort to increase healthcare transparency, the rule required hospitals to publicly disclose the final costs they pay to insurers for services and procedures.

This is just one of several articles we have on the history of insurance regulation. For more fun facts and historical whodunits, check out the rest of the articles in our History of Insurance Regulation series.

To keep up with the regulatory changes that are happening now, see how AgentSync can help.

Get the latest updates on new insurance industry content.

There are many compliance risks that can put an insurance agent…

You can reduce the risks to your core business!

Let Susan in Compliance finally take a vacation.