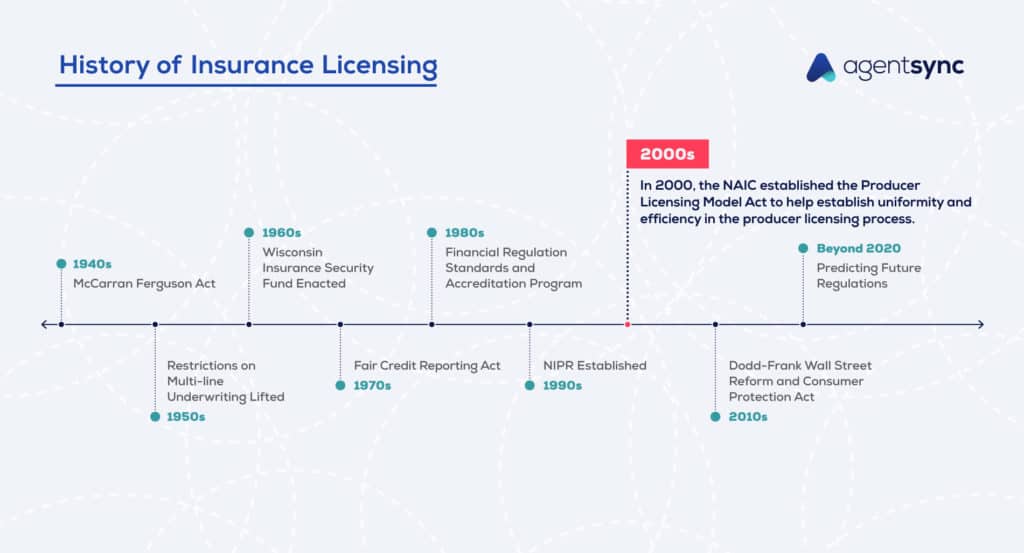

History of Insurance Regulation in the 2000s

CATEGORIES

COMPANY TYPE

As the world changes, so too must insurance regulation. Regulators need to stay on top of the social and economic landscape to ensure the industry works for today’s consumers. That’s as true now as it was through every single decade since 1750 BC – the birth of insurance regulation.

The 2000s are no different – they represent a notable decade in the industry for the positive implementation of uniform policy standards and market conduct oversight. But the tragic events of 9/11 and the 2008 financial crisis shone particular light on how vulnerable everyday Americans were to the inner workings of the financial industry.

Producer licensing is a hot topic in the world of insurance regulation, and one that’s very close to our hearts here at AgentSync.

Producer licensing is important because it helps ensure anyone who sells, solicits, or negotiates insurance in the United States complies with state laws and regulations. But the process of producer licensing can be fairly cumbersome and varies greatly between states.

So, to prevent re-work and unnecessary licensing across states, in 2000, the NAIC established the Producer Licensing Model Act to help establish uniformity and efficiency in the producer licensing process. The model act outlines reciprocity agreements between states, which waives licensing requirements for nonresident producers so long as that producer’s resident state affords the same rights to the resident producer of the state who has adopted the act.

When the Gramm-Leach-Bliley Act was passed in 1999, the idea was to remove regulation that outright bans activities by replacing it with systems of oversight to proactively catch issues before they occur. The ethos here is that adequate oversight could create a reflexive, dynamic insurance industry that would grow with society to better meet changing consumer needs.

Adding a little flexibility to the industry is a beautiful idea, but without the proper oversight systems in place, it can have dire consequences for consumers. In 2002, the Market Conduct Annual Statement was developed to provide state regulators with a uniform system of market conduct analysis. Annual statements, it was determined, are the bedrock to financial regulation. Since many states already engaged in annual market analysis, the creation of the Market Conduct Annual Statement gave structure and cohesion to an existing system.

The Market Regulation and Consumer Affairs (D) Committee held a public hearing in 2002 on the use of credit scores in underwriting and rate-making.

Tasked with addressing the availability and affordability of insurance, the Committee was particularly concerned with the disparate impact underwriting with credit scores may have on protected classes of individuals. This was balanced against the understanding that “there is a correlation between an individual’s insurance bureau score and risk of loss … and scores make underwriting and rating more objective, more complete and more equitable.”

Following the public hearing, many states formed their own independent task forces to assess the use of credit scores and underwriting within their states. What many found was that “neither unfettered use of credit-based insurance scoring nor total ban of credit-based insurance scoring” was an appropriate path forward. Instead, states needed to create proper oversight while simultaneously educating consumers on the issue.

The Sept. 11, 2001, terrorist attacks on the World Trade Center and the Pentagon sent shock waves across the United States as the country came to terms with the immense losses brought on by the attacks. In the aftermath of the attacks, it was estimated that insured losses – including property, life, workers compensation, health, disability, and business interruption – would exceed $47 billion. While the insurance industry is designed to ease the financial burden arising from these losses, the toll of the attacks on families and individuals is something that cannot now nor ever be measurable in dollars.

Prior to the attacks, terrorism insurance was included in most general insurance policies. But due to the losses incurred by the industry, coverage in the instance of terrorism was separated from general policies and became prohibitively expensive for the average consumer.

In response, Congress passed TRIA in 2002 as a temporary program that would allow the federal government to share monetary losses with insurers for commercial property and casualty losses. TRIA has since been renewed four times and is slated for reauthorization in 2027.

In 2003, the prevalence of vulnerable seniors being sold unsuitable annuity products within the industry led to regulators stepping in to establish the Suitability of Annuity Transactions Model #275 and oversee the sale of annuities.

The purpose of the act is to “require producers … to act in the best interest of the consumer when making a recommendation of an annuity and to require insurers to establish and maintain a system to supervise so that the insurance needs and financial objectives of the consumers at the time of the transaction are effectively addressed.” This helps to ensure the product sold to the consumer is the one that best meets their needs, rather than the one that will provide the producer with the highest sales commission.

In the 2000s, the NAIC formed the Speed-to-Market Working Group with the goal of modernizing insurance regulation by driving efficiencies in the insurance policy filing and review process. The Working Group recommended “the development of a system featuring a single point of filing and review; development of national standards for insurance products; and a more efficient state-based procedure for processing and filing.”

To answer that call, the NAIC – in cooperation with state insurance regulators – developed an interstate compact and accompanying legislation through the Interstate Insurance Compact Model. The model legislation was finalized and adopted by the NAIC in July 2003, with Colorado and Utah the first two states to enact it. By May 2006, the threshold of 26 states, or 40 percent of premium volume nationwide, had adopted the model, thus initiating the creation of the IIPRC.

Insurer solvency is an important issue for the insurance industry in general and state regulators specifically. The NAIC regularly updates solvency requirements based on national and global developments to financial solvency tools and regulatory frameworks.

In 2008, the NAIC’s SMI began a self-examination of the “the United States’ insurance solvency regulation framework and includes a review of international developments regarding insurance supervision, banking supervision, and international accounting standards and their potential use in U.S. insurance regulation.”

What the SMI found was, since the regulatory responsibility of insurer solvency lies with state insurance departments and insurers operate between states, the U.S. solvency framework relies on state insurance departments adhering to the accreditation program, which demonstrates a baseline standard for regulation.

Thought we were finally done with the subject of insurer solvency? Think again. The 2008 financial crisis and the collapse of the housing market had a profound impact on the insurance industry, resulting in even more regulatory requirements to manage insurer solvency.

We know that in the ‘90s the NAIC implemented risk-based capital (RBC) to manage the amount of capital insurers needed to take on risk and protect against insolvency. But the assessment of an insurer’s RBC and investment portfolio were tied to credit ratings. And since the collapse of the mortgage-backed securities market exposed great flaws in the rating agency modeling process, the market lost confidence in the Nationally Recognized Statistical Rating Organization and the credit ratings on which the insurance industry previously relied.

As a result, the Structure Securities Project was set up by the NAIC to develop a new financial modeling process to determine RBC standards and mortgage-backed securities held by investors.

Regulatory changes within the insurance industry are both historic and ever-evolving. It can be more than a full-time job to keep on top of which ones apply to your organization when managing regulatory compliance.

This is just one of several articles we have on the history of insurance regulation. For more fun facts and historical whodunits, check out the rest of the articles in our History of Insurance Regulation series.

To keep up with the regulatory changes that are happening now, see how AgentSync can help.

Get the latest updates on new insurance industry content.

There are many compliance risks that can put an insurance agent…

You can reduce the risks to your core business!

Let Susan in Compliance finally take a vacation.