A History of Modern Insurance Regulation Through the Ages

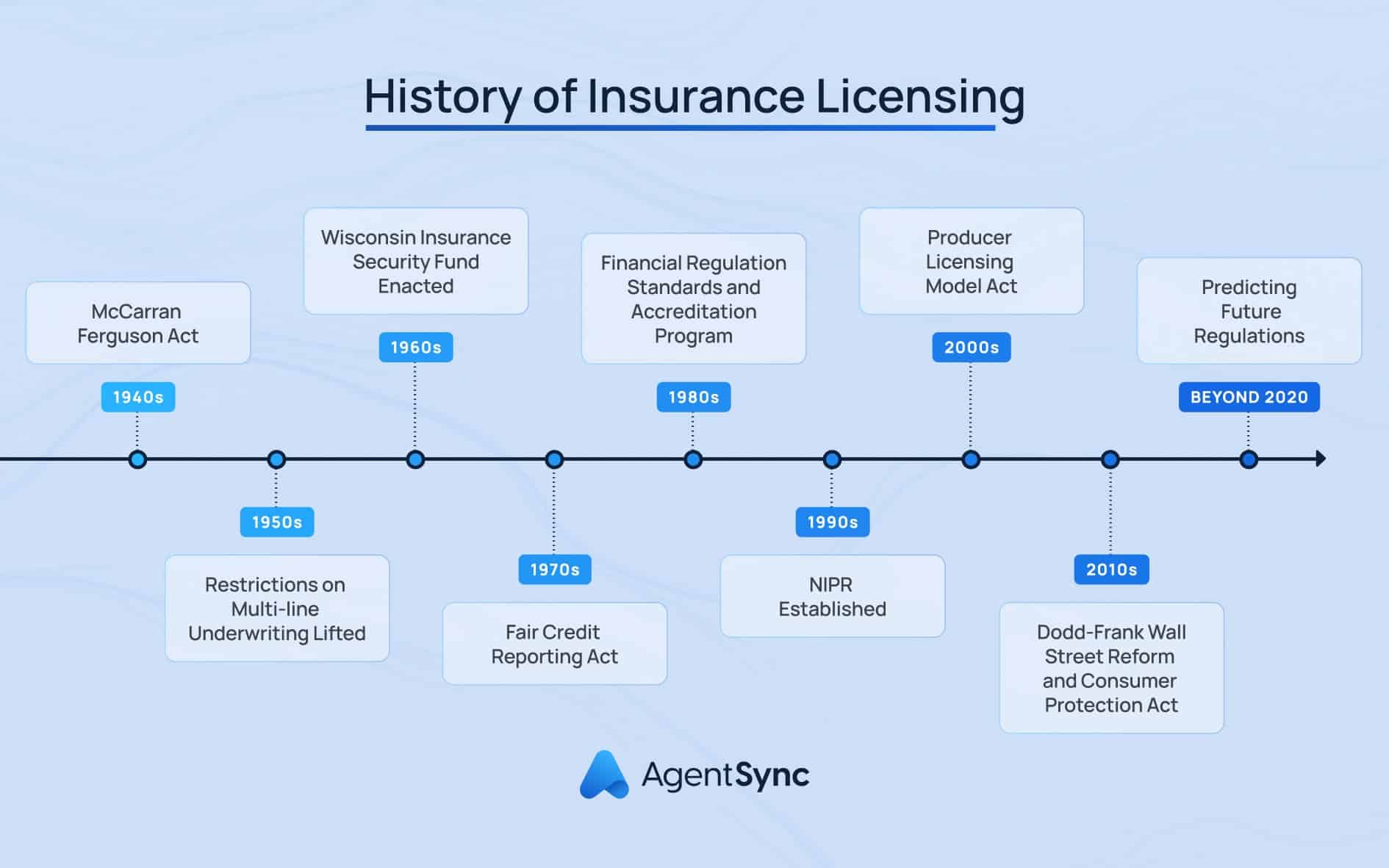

Laws, rules, and regulations in the insurance industry are nothing new. On the contrary, the insurance industry has been highly regulated as far back as the McCarran-Ferguson Act of 1945, which gave the power to regulate the insurance sector to individual states.

Each state has its own set of rules and laws regulating the insurance sector, enforced by the state department of insurance. Because laws differ across 50 states, the District of Columbia, and multiple U.S. territories, insurance agents, brokers, and carriers must juggle more than 50 distinct sets of rules.

With each new presidential election, the pendulum swings back and forth. Some administrations are more focused on protecting consumers at the expense of the free market and insurance company profitability. Others deregulated the insurance industry, leaving state departments of insurance to take charge of protecting consumers.

In our Regulatory Changes in the Insurance Industry series, we’ll explore, decade by decade, the U.S. insurance compliance landscape and its changes over time.

Where it all began

Physical evidence of insurance regulation dates as far back as 1755-1750 B.C. to an ancient Babylonian legal text called the Code of Hammurabi.

In Babylon, seafaring merchants would fund their shipments through loans. By paying lenders an added fee – read: premium – the lender would agree to cancel the loan in the instance of a lost or stolen shipment.

The Code of Hammurabi presents consequence scenarios for those who fail to adhere to the rule of law, including the above-mentioned loan forgiveness, and identifies King Hammurabi’s responsibility to prevent the strong from oppressing the weak.

We aren’t in Babylon anymore

While insurance regulation has changed in the years since Babylon, the function of insurance and the key purpose of its regulation is essentially the same: to protect consumers from oppressive corporate behavior when managing risk.

In the U.S., that effort is championed by the National Association of Insurance Commissioners (NAIC). Founded in 1871, the NAIC provides support, collaboration, and guidance to insurance regulators across the country.

But the birth of our modern state-based regulatory framework was really in 1945 with the McCarran Ferguson Act. This is a noteworthy turning point for insurance regulation in the U.S. because it solidifies the state’s responsibility to keep a pulse on local consumer needs.

What does this mean for the industry?

States have the power to establish different rules across the insurance industry, including policy details and licensing requirements. Whether you’re buying an insurance policy or looking to sell insurance in a given state, you’re impacted by state regulatory requirements for insurance.

Before we hear a bah humbug for insurance regulation, it’s important to remember that states build their regulatory framework to protect consumers. For instance, Louisiana state regulators are best placed to create regulation for property and casualty insurance policies in Louisiana because they’re uniquely accustomed to the same disasters that threaten Louisiana consumers’ property: hurricanes and floods. A Kansas state regulator may not be so acutely attuned to the challenges facing Louisiana.

So, while regulatory changes may seem like a pile of bureaucracy, they’re important to ensure the industry stays relevant when meeting consumer needs. But that doesn’t make them any easier to stay up to date with.

Regulatory changes within the insurance industry are both historic and ever-evolving. It can be more than a full-time job to keep on top of which ones apply to your organization when managing regulatory compliance.

If your business is ready to use modern technology to solve this pain point and automate much of the compliance process, check out AgentSync in action.

This is just one of several blogs we have on the history of insurance regulation. For more fun facts and historical whodunits, check out our ongoing series, Regulatory Changes in the Insurance Industry.

History of Insurance FAQs

1. Why do we need insurance regulatory requirements?

Regulatory requirements may seem like an arbitrary labyrinth, but there’s a method to this madness, we promise. Regulators spend a lot of time studying market trends, identifying sticking points in the industry, and clearing a path forward for a productive, more efficient insurance industry. Regulatory requirements are designed to help producers, MGAs/MGUs, agencies, and carriers stay on the up and up while doing what’s best for the country’s consumers.

2. Why do insurance regulatory requirements change?

As society changes, so too must regulatory requirements. After all, they’re designed to protect consumers from the current issues plaguing the insurance industry. Consider, for example, the rise of insurtech. As the insurance industry adopts emerging technologies, it brings about a series of implications that previously didn’t exist – data security, real-time virtual access to producers, etc.

3. Who makes insurance regulatory changes?

Changes in the insurance industry can be influenced by any number of sources. For instance, if the federal government enacts a new law that impacts the insurance industry, state insurance departments will respond with insurance regulation. That said, in the United States, the insurance industry is regulated on a state-by-state framework, meaning the states have control over their own regulatory requirements.

4. What happens if you don’t keep up with insurance regulatory changes?

Bad news bears. A failure to keep up with regulatory changes can result in costly regulatory actions. It isn’t fun for anyone involved, trust us.