History of Insurance Regulation In The 1980s

CATEGORIES

COMPANY TYPE

Changes to insurance regulation help ensure the industry works in the best interest of consumers. While regulations may be built with the best intentions, if they don’t perform as they’re meant to, then they need to change.

The 1980s are marked by industry-wide improvements across many facets of insurance regulation, including privacy protection, mortality tables, and accreditation standards. What’s particularly noticeable about these changes is the collaboration across the federal government, the NAIC, and state regulators that brought them into existence.

In the 1980s, the NAIC released the Insurance Information and Privacy Protection Model Act and accompanying amendments to provide legislation at the state level for protecting individuals’ personal information.

At the time, consumer privacy was a hot-button issue. At the federal level, the Fair Credit Reporting Act had already passed and the U.S. Privacy Protection Study Commission (PPSC) had spent the 1970s studying “data banks, automated data processing programs, and information systems of governmental, regional, and private organizations, in order to determine the standards and procedures in force for the protection of personal information.” And within that purview fell the insurance industry.

In developing the Insurance Information and Privacy Protection Model Act, the NAIC relied heavily on the findings of the PPSC. Central to the PPSC’s final report was the argument that the relationship between the insurer and the insured should guide the standards of data collection, use, and disclosure, rather than abstract government regulations. It’s a statement which rings with its own air of the abstract.

Ultimately, personal information is central to the insurance industry. Insurers rely on customer data when assessing risk and building policies. But the need in the industry for personal data shouldn’t inherently put customers at risk of data leaks. So the process of writing the Insurance Information and Privacy Protection Act was extremely delicate. The NAIC needed to walk a fine line between “(1) the legitimate needs of the insurance industry for information and (2) the public’s need for fairness in insurance information practices and protection of personal privacy.”

When the NAIC introduced separate male and female mortality tables in the 1970s, it was met with mixed reviews. While the separate tables could help insurance companies more accurately manage reserves and price premiums, it also resulted in gender-biased decisions within the industry. Some states answered this issue by making the use of separate male and female mortality tables illegal.

In 1983, the NAIC approved gender-blended mortality tables for inclusion in model laws and regulations. In response, many states adopted the model regulation.

This is important because it demonstrates the role of the NAIC to support state regulators as they build the regulatory requirements best suited to their states and their states’ consumers. Additionally, by creating gender-blended mortality tables, the NAIC supported uniformity among states in the regulation of life insurance products. Had NAIC stuck to separate male and female mortality tables, then the states that had deemed their use illegal would have varied greatly in regulation from those who supported their use.

State regulators are in charge of creating and managing regulations within their own states because they know the issues that impact their state better than anyone. But often insurance companies operate across state lines. These multi-state insurers need to meet regulatory requirements for every state within which they operate. But it’s also up to the state to perform the level of oversight necessary to hold insurers accountable.

This creates something of a regulatory nightmare. Insurers don’t want to waste time dealing with audits and financial examinations by every single state within which they operate. But if state regulators don’t make sure the insurers operating within their state are meeting regulatory requirements, then the consequences can be dire. The ‘80s offer a prime example of this.

In the mid-late 1980s, a number of multi-state insurance companies became insolvent. Consumers are often protected by guaranty funds, which cover the cost of insured claims in the instance of insurer insolvency. However, widespread industry insolvency doesn’t do much to build consumer confidence.

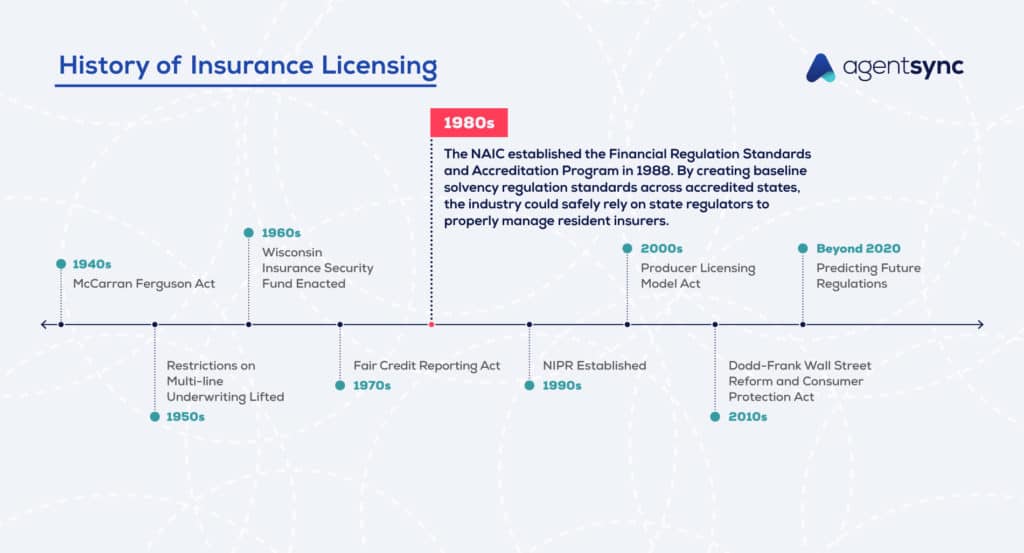

To answer this problem, the NAIC established the Financial Regulation Standards and Accreditation Program in 1988. By creating baseline solvency regulation standards across accredited states, the industry could safely rely on state regulators to properly manage resident insurers. That way, regulators wouldn’t need to hold their own financial examinations of the nonresident insurers operating within their state.

Today, all 50 states, the District of Columbia, Puerto Rico, and the U.S. Virgin Islands are accredited.

Regulatory changes within the insurance industry are both historic and ever-evolving. It can be more than a full-time job to keep on top of which ones apply to your organization when managing regulatory compliance.

This is just one of several articles we have on the history of insurance regulation. For more fun facts and historical whodunits, check out the rest of the articles in our History of Insurance Regulation series.

To keep up with the regulatory changes that are happening now, see how AgentSync can help.

Get the latest updates on new insurance industry content.

There are many compliance risks that can put an insurance agent…

You can reduce the risks to your core business!

Let Susan in Compliance finally take a vacation.