History of Insurance Regulation In The 1960s

CATEGORIES

COMPANY TYPE

In previous decades, we saw the insurance industry build a robust framework of state-based regulation. The 1960s offered a new era in insurance.

With the groundwork already laid, the insurance industry spent the decade of the 1960s starting to identify and fill key gaps in both policy coverage and regulatory consumer protections.

Beyond regulatory changes, the NAIC also developed the Center for Insurance Policy and Research to archive and protect information on regulatory changes through the years. Today, it’s an important resource to drive understanding of insurance issues and discussion as to the future of insurance policy.

The New York State Insurance Department appointed the Special Committee on Insurance Holding Companies in 1967 following noticeable interest among insurance industry executives to enter into holding company arrangements.

A holding company is a company that controls the majority stock of a different company. The holding company doesn’t produce anything, sell anything, or conduct any business other than holding controlling stock in subsidiary companies. It’s a corporate mechanism and unsurprisingly, sometimes corporate mechanisms have major implications for the public interest.

The holding company arrangement has the potential to allow companies to diversify product lines, maximize earnings, and increase business efficiencies. But it also allows companies to “free assets and investments from the regulatory control of the insurance laws, or to avoid the operation of specific insurance laws… or to save on taxes.”

So, while holding companies do have the potential to bolster the insurance industry, the Special Committee on Insurance Holding Companies reported it was more of a “yes, but” situation. Yes, holding companies are a good idea for insurance, but only with the appropriate level of regulation and oversight.

The NAIC responded shortly after (1968) by forming the Subcommittee to Draft Model Legislation Relating to Insurance Holding Companies. It was a subcommittee tasked, unsurprisingly, with drafting model legislation for states on the issue of holding companies. Central to this model legislation were the research and findings that came from New York’s Special Committee on Insurance Holding Companies.

Historically, floods were considered something of an uninsurable risk. With insufficient data to measure the frequency and severity of flood risks, private insurers couldn’t reconcile the risk of staggering losses with the benefit of offering a much-needed insurance policy.

But a lack of private flood insurance doesn’t stop floods from happening. In the 1960s, frequent flooding and a lack of flood coverage through private insurance put pressure on the federal government for disaster assistance.

In 1965, when Hurricane Betsy caused widespread damage across Florida and Louisiana – the cost of which was estimated as high as $1.5 billion – the federal government decided to step in and take on the job of selling flood insurance.

Founded in 1968, the NFIP was managed by the Federal Emergency Management Administration (FEMA) and was tasked to “provide flood insurance, to improve floodplain management, and to develop maps of flood hazard zones.” Still around to this day, the NFIP helps to offset the potentially devastating cost of floods by providing affordable flood insurance to those in areas most at risk.

An annuity is a type of insurance policy where, by paying an upfront fee – either as a lump sum or a series of installments – consumers (annuitants) can receive regular payments for a predetermined amount of time. Simply put, annuities help to ensure a constant revenue stream for the annuitant.

But the amount of money that an annuitant receives depends on the payout rate, which is determined by the annuitant’s expected mortality risk (more on this in the next decade) and the rate of return on the contract. Since payout rates depend on a number of factors, including the annuitant’s age, gender, and initial contribution, there’s a lot of inconsistency between annuity terms. Some contracts, called “variable annuities,” even offer returns based on actual investments in stock portfolios and mutual funds instead of as consistent percentages or guaranteed returns.

Annuities have existed long before the 1960s, but they gained renewed regulatory relevance due to the 1959 Supreme Court ruling SEC v. Variable Annuity Life Insurance Co. of America. In it, the Supreme Court found that variable annuities, because of their invested component, should be classified as securities rather than insurance, and, therefore, those selling variable annuities should be registered with the Securities and Exchange Commission (SEC) and regulated under the Investment Company Act of 1940.

In response, the NAIC collaborated with the SEC to establish a uniform method for regulating and reporting on variable annuity activities within the industry. As part of that collaborative effort, the NAIC put together model legislation to help states navigate the complexities of the securities regulation of variable annuity contracts.

Sure, we pay our premiums to insurers, but how can we be sure they’ll pay our claims when we need them to, especially in the instance of an insurer facing bankruptcy.

The answer: guaranty funds.

Guaranty funds protect insured policyholders by paying out claims regardless of the financial situation of an insurer. It ensures policyholders won’t be left high and dry at the very moment they need their insurer due to irresponsible business practices.

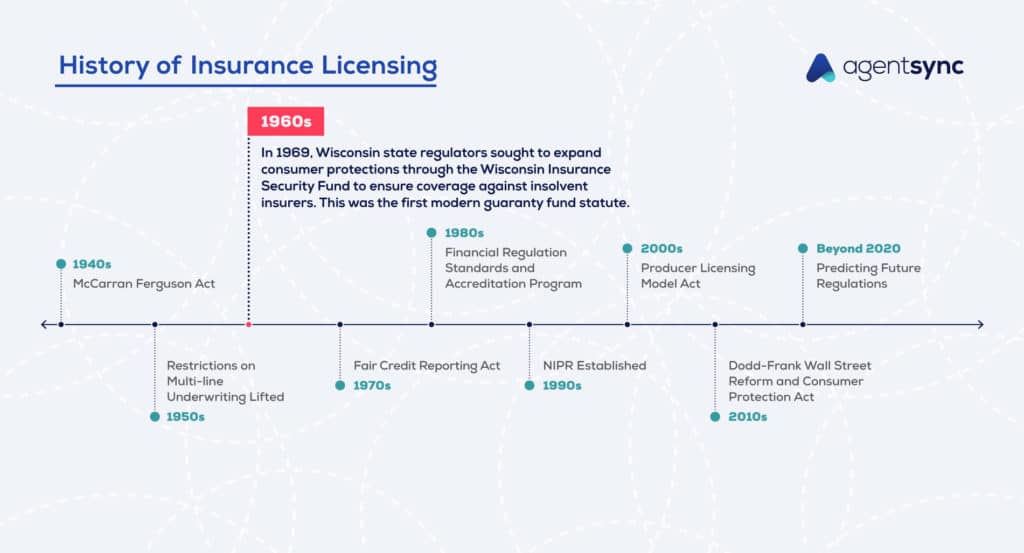

In 1969, Wisconsin enacted the first modern guaranty fund statute into their state regulation. Wisconsin state regulators sought to expand consumer protections through the Wisconsin Insurance Security Fund (the Fund) to ensure coverage against insolvent insurers.

As explained by the Fund, its purpose is to “maintain public confidence in the promises of insurers by providing a mechanism for protecting insureds in this state from excessive delay or loss in the event of liquidation of insurers and by assessing the cost of such protection among insurers.”

It also became the basis for language in the NAIC Model Rehabilitation and Liquidation Act. A document that provides model legislation for states to adopt when looking to create their own guaranty fund to cover consumer claims through insurer insolvencies.

In 1969, the NAIC established the Center for Insurance Policy and Research. This research arm of the NAIC includes the addition of the NAIC library.

A valuable source of information for all stakeholders in the insurance industry – we’re talking policymakers, commissioners, regulators, industry experts, insurance professionals, and academics – the Center for Insurance Policy and Research is now available as an online database for research and education.

Regulatory changes within the insurance industry are both historic and ever-evolving. It can be more than a full-time job to keep on top of which ones apply to your organization when managing regulatory compliance.

This is just one of several articles we have on the history of insurance regulation. For more fun facts and historical whodunits, check out the rest of the articles in our History of Insurance Regulation series.

To keep up with the regulatory changes that are happening now, see how AgentSync can help.

Get the latest updates on new insurance industry content.

There are many compliance risks that can put an insurance agent…

You can reduce the risks to your core business!

Let Susan in Compliance finally take a vacation.