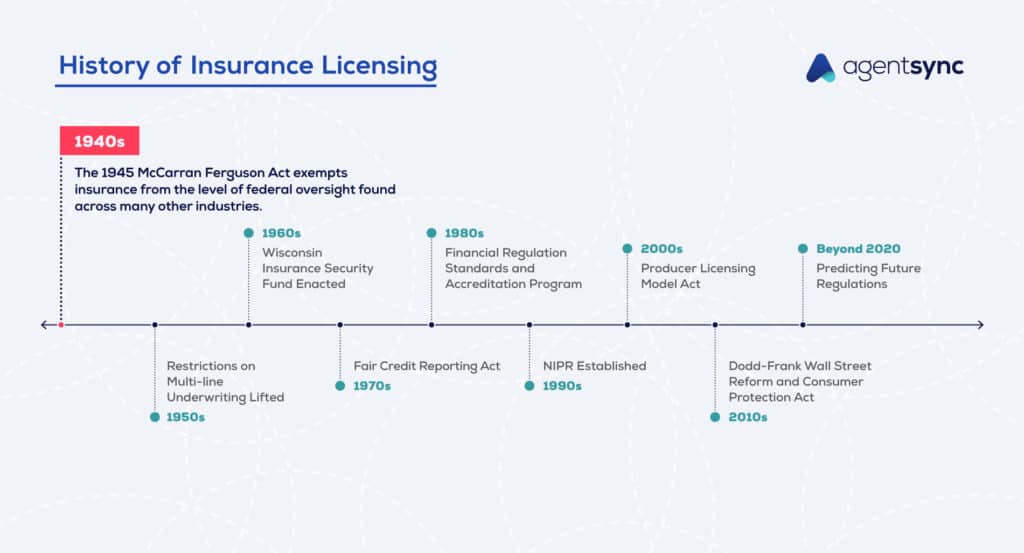

History of Insurance Regulation In The 1940s

CATEGORIES

COMPANY TYPE

Have you ever wondered how the U.S. framework for modern insurance regulation came into existence? Don’t lie to us, we know you have!

Even if the birth of state-based insurance regulation doesn’t keep you up at night, understanding how insurance regulation evolves over time can go a long way toward helping you understand recent changes and potential changes in the future.

And it all begins right here, in the 1940s.

Simply put, the 1945 McCarran-Ferguson Act exempts insurance from the level of federal oversight found across many other industries. But the basis of the 1945 McCarran-Ferguson Act can be traced all the way back to the early 1850s, when states started to appoint state insurance commissioners.

Historically, insurance wasn’t considered “commerce” – the exchange of goods and services – in the sense of the term as outlined in the Commerce Clause in the U.S. Constitution. Since insurance couldn’t be classified as commerce, states had the freedom to create rules and regulations as they liked. But the state-based regulatory system is sometimes complicated and hard to adhere to, so insurers attempted to undermine the industry’s state-based regulatory system by having insurance classified as commerce.

It may seem pedantic, but the classification of insurance as commerce – or not – has far-reaching legal consequences. The Commerce Clause gives the United States Congress (the federal government) the power to regulate commerce and, in turn, limits state involvement.

So, in the 1869 court case Paul v. Virginia, the U.S. Supreme Court ruled insurance is not commerce, solidifying the role of the states in insurance regulation by removing insurance from Congress’ legislative reach. That ruling lasted all the way until 1944, when the U.S. Supreme Court overturned Paul v. Virginia with the United States v. South-Eastern Underwriters Association. By designating that insurance does indeed fall within the Commerce Clause, the U.S. Supreme Court placed insurance within the purview of Congress, thus threatening the state-based regulatory system.

In direct response, Congress enacted the McCarran-Ferguson Act of 1945, limiting the applicability of antitrust laws in the case of insurance and protecting the states’ regulatory authority in the industry.

Et voilà, the state-based regulatory system that we know and love lives on.

In 1946, the NAIC introduced two model rating laws – one for property and one for casualty – to provide guidance as to how insurance policies should be written and priced.

Pricing insurance rates can be complicated because insurers need to set premium prices before they know the true cost of the insurance coverage. An actuary will try to predict the cost of future losses based on available historical data. But ultimately, insurance rate making is an assumption based on a statistical analysis of risk and price competition between insurers.

The two model rating laws introduced the actuarial and regulatory responsibility to ensure premium rates don’t become prohibitively high for consumers, too low to cover the true cost of coverage, or unfairly discriminatory. Although these model laws have been amended and changed slightly since the ‘40s, the overall point remains the same: “to improve availability, fairness and reliability of insurance.”

The ‘40s were a big decade for model legislation. In addition to establishing model rating laws across property and casualty, the NAIC also adopted the very first version of the Unfair Trade Practices Act.

The Unfair Trade Practices Act prohibits businesses from using unfair or deceptive tactics when selling insurance policies across life, health, and property and casualty insurance. As with most regulations, the goal is to protect consumers from unethical business practices. As a result, the Unfair Trade Practices Act provides model legislation that states can adopt and tweak to meet their specific expectations for interstate trade practices.

The model legislation defines unfair trade practices as including, but not limited to, the misrepresentation and false advertising of insurance policies, boycotts, coercion, intimidation, and discrimination.

It’s important to remember that while the NAIC provides these model legislations to states as a jumping-off point when creating state-based regulations, states have the flexibility to amend and update the legislation as they see fit. Relying exclusively on the NAIC model regulations (and unknowingly trespassing state-specific rules) can open insurers up to regulatory actions. This makes it doubly important to always refer to state-specific legislation when managing insurance compliance in any state of operation.

The McCarran-Ferguson Act and model rating laws establish important guidelines for the regulation of the insurance industry and the protection of consumers.

Although the industry has changed since the 1940s, the relevancy of these regulatory movements remains the same. Without the McCarran-Ferguson Act, the regulatory system could be one led and managed by the federal government, and that would be problematic since states are the ones best placed to address unique state-by-state regulatory challenges. And while the verbiage in model legislation iterates slightly through the years, the purpose remains unchanged: to protect consumers from oppressive business practices.

Regulatory changes within the insurance industry are both historic and ever-evolving. It can be more than a full-time job to keep on top of which ones apply to your organization when managing regulatory compliance.

This is just one of several articles we have on the history of insurance regulation. For more fun facts and historical whodunits, check out the rest of the articles in our History of Insurance Regulation series.

To keep up with the regulatory changes that are happening now, see how AgentSync can help.

Get the latest updates on new insurance industry content.

There are many compliance risks that can put an insurance agent…

You can reduce the risks to your core business!

Let Susan in Compliance finally take a vacation.